When Shannon Johnson-George’s personal laptop went bust in February, she decided not to spend the roughly $1,000 it would cost to replace it. She plans to rewear an old dress for her son’s college graduation next month after being shocked by the $100-plus prices at the online retailers she frequents. Yet over the next five months, the 40-year-old from Cincinnati has a Disney cruise, a visit to Lake Erie and a trip to New Orleans for a Bruno Mars concert booked.

Johnson-George and her husband, Chris, aren’t struggling. They are cutting back where they feel prices have risen too far—primarily the stuff that fills their closets, living room and garage. “We’re trying to spend more on activities because we’ll always remember them,” Johnson-George said.

Across the American economy, consumers are making similar calculations. They are still spending—many flush with cash from tax refunds—but how they spend is changing. Shoppers are spending less on goods like clothing, furniture and sports equipment, which have risen in price over the past year. At the same time, they are spending more on some services and experiences, like travel and healthcare.

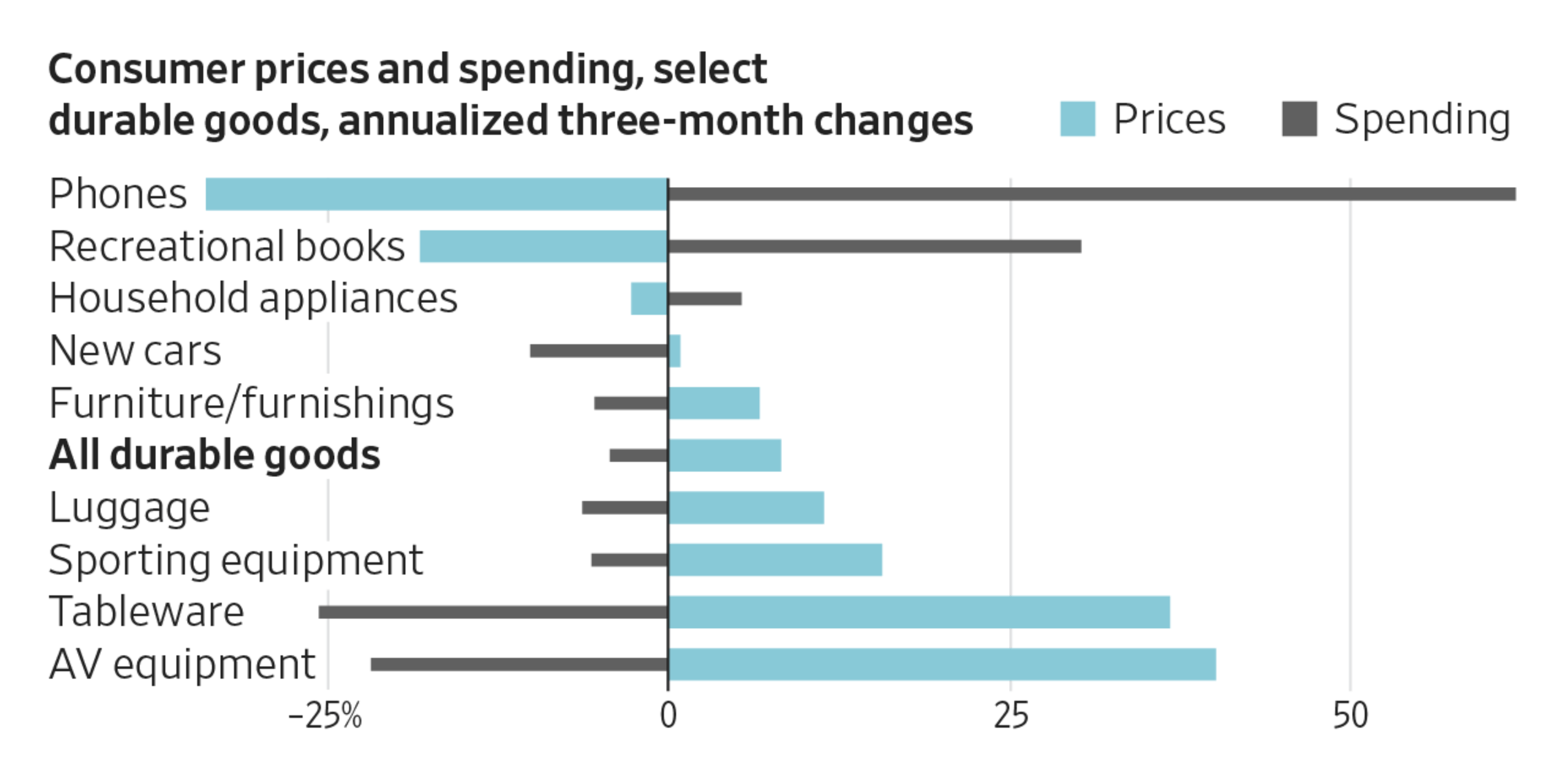

The latest consumer-spending data from the Bureau of Economic Analysis, which runs through February, shows that many of the goods for which prices have risen fastest are the same ones for which spending, adjusted for inflation, is falling most.

Spending on clothing fell about 7% between December and the end of February, after adjusting for seasonal variations like holiday shopping and projecting the trend across a full year. Clothing prices were up 9% over the period. Using the same methodology and time frame, furniture buying was down 5% as prices were up 7%. And sporting-equipment purchases were down 6%, with prices up 16%.

“At the end of the day, goods spending is weak and goods prices are up,” said Renaissance Macro Research economist Neil Dutta, who flagged the correlation. “It’s very simple.”

The dynamic is important because it reveals a weakness not evident in the broader data: Consumers are pulling back where price increases on goods are most dramatic. Consumer spending in aggregate appears to be holding up, a sign that some say shows inflation isn’t having that much effect despite widespread complaining. Under the surface, inflation’s impact is clear.

To Dutta, this situation is different from the inflation of the Covid era, when increased demand, consumers flush with cash, and supply-chain shortages sent prices skyrocketing. Now, Dutta said, it isn’t strong demand pulling prices up but other factors largely around tariffs and supply-chain pressures. Companies, he said, are seeing more resistance to price increases.

Consumers aren’t cutting back everywhere that prices are rising. They are still spending on travel, financial services and healthcare services, for example, even though prices are up.

Last week, retailers posted strong sales in March, driven in part by higher gas prices. EY-Parthenon chief economist Gregory Daco said the numbers indicate that consumers are holding up for now, likely cushioned in part by larger tax refunds. But he expects inflation to slow spending going forward. Restaurant spending rose only 0.1% in March from February, according to the retail sales report. Prices for dining out rose 0.2% during that time.

“What you’re seeing is that the higher tax refunds are partially offsetting the higher gasoline prices,” Daco said. But consumers are still facing an environment where income growth is slowing and prices are rising, “and that will limit their ability to spend going forward.”

For now, that means families with some level of disposable income are making constant trade-offs and negotiations about where and how to spend.

Nick and Rachel Lahlum went on a roughly $5,000 trip to Cozumel, Mexico, in January. The couple, who live in Anoka, Minn., with their two children, have never eaten so much steak after buying a quarter cow from a local farm for $950 to keep in their freezer, plus a whole hog.

But the Lahlums, who own a home and bring in combined salaries of around $115,000, are re-evaluating elsewhere. They are installing a patio themselves instead of hiring someone to do it. They are growing vegetables to offset their grocery bill. And Rachel, who runs a wedding-photography business, is holding off on buying new camera lenses. (Prices for photographic equipment and supplies are up 12% over the past year, according to the Labor Department.)

“I need to be able to pay myself if I don’t find as much work as I have over the past five years,” the 36-year-old said, adding that she is still booked through the summer.

Chicago financial adviser Michael Biggus said many of his clients are cutting back on discretionary purchases, even those with healthy savings and incomes.

He has made some spending trims himself, not because he needs to tighten his belt but because some purchases are beginning to feel wasteful as prices rise. Biggus, 64, and his wife, an archivist, make over $200,000 a year. They own their lakefront condo outright and have no children. When restaurant prices at their regular spots started nudging up, they adjusted their orders. Instead of getting a glass of wine each and perhaps an appetizer to split, they now stick to water and an entree apiece to get out the door for under $70.

“It’s not that we don’t have the money,” said Biggus. “It’s that we don’t like frittering it away.”

Write to Rachel Wolfe at rachel.wolfe@wsj.com